UPI - 8 Key Metrics You Should Know!

Introduction

UPI, or Unified Payments Interface is a real-time payment system developed by the National Payments Corporation of India (NPCI) which is regulated by the country’s apex Bank “The Reserve Bank of India”.

Launched in 2016, It has revolutionised digital payments in India, making it one of the fastest-adopted payment systems in the world. It has gained widespread popularity in India due to its convenience, security, and interoperability across different banks and financial institutions.

My Blog Post highlights the 8 Metrics you should know when using UPI.

Table of Contents

What is UPI

UPI or Unified Payments Interface facilitates convenient and secure instant fund transfer by allowing users to transfer money instantly between two bank accounts on a mobile platform, without requiring any details of the recipient’s bank. allows users. It enables users to make interbank peer-to-peer (P2P) and person-to-merchant (P2C) transactions using a Virtual Payment Address (VPA) linked to a bank account or a credit card.

What is VPA in UPI

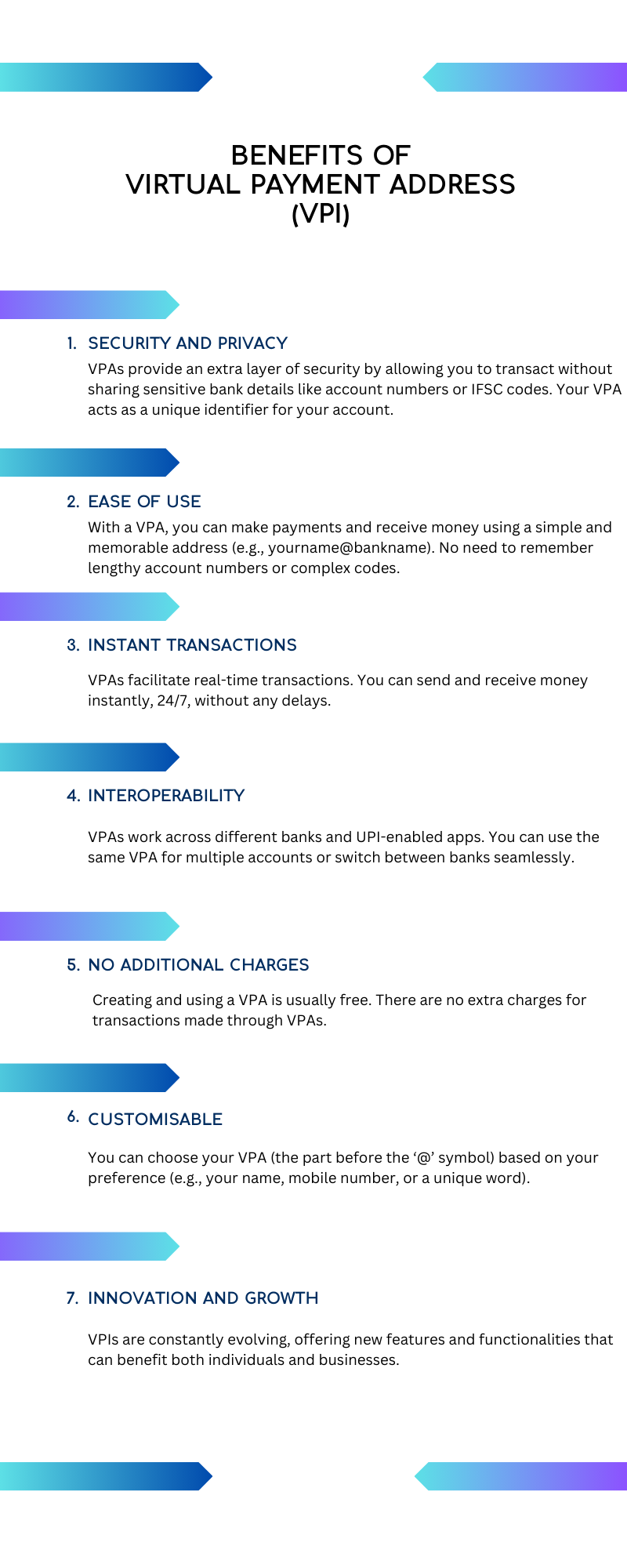

VPA stands for Virtual Payment Address. It is a unique identifier used in the Unified Payments Interface (UPI) system playing a crucial role in its functionality.

What it is :

- A VPA is an ID independent of your bank account number and other details.

- It helps UPI track a person’s account.

- You can use a VPA to make and request payments through a UPI-enabled app.

- With a VPA, you don’t need to fill in your bank account details for multiple payments repeatedly.

- A typical VPA looks something like abc@bankname, where ABC can be anything (such as your name or mobile number), and the bank name refers to the associated bank or just the word “UPI”

- Each bank account linked to UPI can have its own VPA, often customizable to your preference.

To create a VPA of your choice:

- Download and Open the UPI app on your mobile device.

- Go to the ‘Profile’ tab.

- If you’ve already set a VPA, click on the arrow to the right.

- Click the ‘+’ mark to create a VPA.

- Choose the first part of the VPA (before the ‘@’ symbol) from the recommendations or type your desired VPA.

- Confirm the VPA creation.

Note: It is essential to link your VPA to a bank account before initiating any UPI transaction. Always ensure that the mobile number linked to your Bank account matches with the one registered for UPI.

Benefits of Virtual Payment Address in UPI

What is UPI Pin

A UPI PIN stands for Unified Payments Interface Personal Identification Number. It is a 4 or 6-digit code set by users either during UPI registration or later in a UPI application. It serves as an additional layer of security for all your UPI transactions.

Key Features :

- Authentication: Similar to an ATM PIN, your UPI PIN is required to confirm and authorize every transaction you make through a UPI app. It serves as an authorisation code entered by you to confirm every payment made via UPI and prevent unauthorized access to your funds.

- Security: UPI PIN is unique to each account and ensures that only the account owner can authorize transactions. Since you don’t share your UPI PIN with anyone, even if someone knows your VPA (virtual payment address), they can’t initiate transactions without the PIN.

- Multiple uses: Your UPI PIN can be used for various UPI transactions, including sending and receiving money, bill payments, and online shopping.

- Confidentiality: Never share your UPI PIN with anyone to avoid the risk of fraud.

Note: Please note that your UPI PIN holds control over the funds in your bank account, so keep it secure.

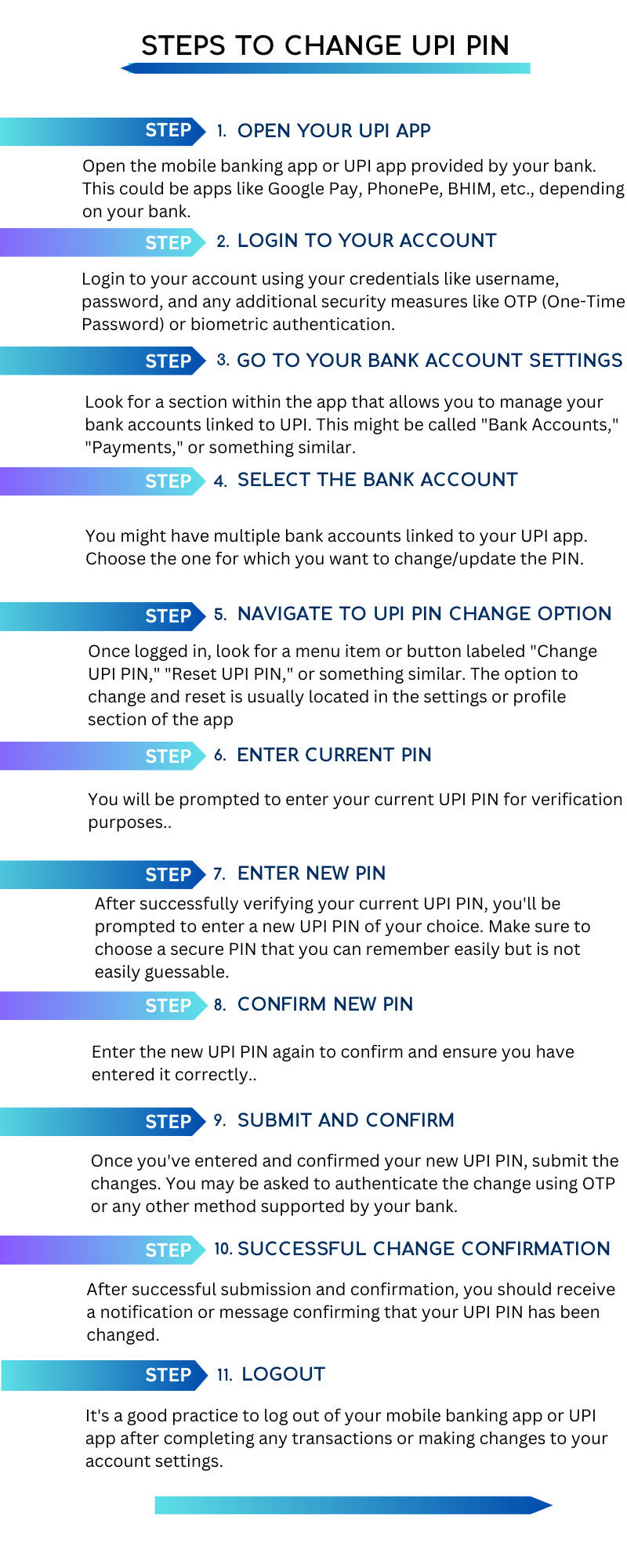

How to Change UPI Pin

To change your UPI (Unified Payments Interface) PIN, you typically need to follow these steps, which may vary slightly depending on your bank’s app or the UPI app you’re using.

Note :

- Always remember to keep your UPI PIN confidential and do not share it with anyone, not even friends, family, or bank representatives. If you suspect that your UPI PIN has been compromised, change it immediately and report any unauthorized transactions to your bank

- Always choose a strong and unique PIN that you don’t use for any other accounts.

- Don’t write down your PIN anywhere where others can see it.

If you forget your PIN, you can usually reset it through your UPI app by following the “Forgot UPI PIN” or similar instructions.

What are UPI Charges

UPI charges differently for individuals and merchants.

For Individuals:

- Generally free: As of today, you won’t face any charges for personal UPI transactions, regardless of the amount. This includes transferring money between bank accounts and making merchant payments (except for specific categories covered below).

- P2M transactions above ₹2,000 with PPIs: Starting April 1st, 2023, a peer-to-merchant (P2M) transaction above ₹2,000 made through Prepaid Payment Instruments (PPIs) like mobile wallets will attract an interchange fee of up to 1.1% However, you, the individual, won’t bear this charge. The merchant accepting the payment through your PPI will be responsible for paying it.

For Merchants:

- Standard charges: While individuals are generally exempt, merchants accepting payments through PPIs for transactions above ₹2,000 might need to pay an interchange fee of up to 1.1%. This fee covers processing, accepting, and authorizing transaction costs, similar to the merchant discount rate for credit cards.

- Interchange Fees: The interchange fee varies based on the type of service:

- Fuel payments: 0.5%

- Post office and telecom payments: 0.7%

- Utilities, agriculture, and education payments: 0.7%

- Supermarket payments: 0.9%

- Insurance, mutual funds, government, and railways: 1.0%

- No Charges for bank-to-bank transactions: No charges will apply If a merchant accepts UPI payments directly from your bank account (not through a PPI)

Note:

- Always confirm the fee structure directly with the merchant before making a large P2M transaction through a PPI.

- For the latest information on UPI charges and guidelines, log in at https://www.npci.org.in/

What is Fake UPI Payment

A Fake UPI payment is a deceptive scheme designed to trick you into thinking you’ve received or made a legitimate UPI transaction, leading to financial losses. These scams can take various forms.

Here are some common types of fake UPI payment frauds:

- Phishing emails or messages: Phishing is one of the most prevalent UPI transaction frauds. You might receive emails or messages from fraudsters pretending to be legitimate entities such as banks or payment apps. These emails or messages may contain fake links that claim to be related to your UPI account or a refund process. Hackers may steal your personal information if you click on these links or unknowingly enter your details (passwords or PINs).

- Fake offers or deals: Scammers might advertise unbelievable deals or offers online and ask for payment from you through UPI. They will deceive unsuspecting buyers like you by either selling counterfeit products or processing orders without delivering the actual product leading to financial losses.

- Fake payment screenshots: Fraudsters exploit screen monitoring apps to create counterfeit screenshots of UPI payment confirmations and send them to unsuspecting users, making them believe they have received a payment. These apps will record screen activities without your knowledge, capturing sensitive information like UPI PINs and OTPs. They might use this tactic to pressure you into sending them “refunds” through a fake link or request your personal information.

- Malware: Malware is a common form of UPI fraud. It can be inadvertently downloaded from fake email attachments or unsecured websites or malicious apps. These will generate fake QR codes that, when scanned and steal your UPI credentials (PIN, OTP). These websites might look similar to your actual UPI app, further adding to the deception.

- Impersonation scams: Fraudsters pose as trusted individuals or organizations, like bank representatives or customer service personnel, and try to trick you into revealing your UPI PIN or OTP. They might call you, send messages, or even create fake social media profiles to appear legitimate.

Note :

- Always stay informed and be vigilant. Being vigilant is crucial to avoid falling victim to UPI fraud.

- Regularly change your UPI PIN.

- Always educate yourself on common phishing scams to take preventive measures.

Top 10 UPI Apps In India

Conclusion

In Conclusion, Unified Payments Interface (UPI) has emerged as a revolutionary digital payment system in India. It is driving the country’s transition towards a cashless economy and fostering financial inclusion by providing access to modern banking services for all segments of society. UPI offers you a seamless, instant, and secure way to transfer funds between bank accounts. It also provides you with a user-friendly interface, speed, and security making it a preferred choice for millions of individuals like you and businesses for conducting financial transactions.

FAQ

What happens if a wrong UPI PIN is entered?

If you enter a wrong or an incorrect UPI PIN, the transaction you initiated will fail.

Are UPI transactions possible only during bank business hours?

No, UPI transactions can be done 24/7 at any time of the day. They are not restricted to bank business hours.

Money has been debited from my account, but I haven’t received any confirmation message. What should I do?

- Whenever a transaction is completed , a success message shows up on the Mobile App. An SMS will also be sent to your registered mobile number from your bank. If you do not receive a payment confirmation within an hour, consider contacting your bank’s customer support.

Is there a way to view my transaction history?

Yes, You can view your transaction history in all UPI Apps. You must access your UPI app’s Home screen and choose the ‘Transaction History’ option to see all your past and pending transactions.

Must I add a beneficiary before making a fund transfer via UPI?

No, unlike NEFT transactions, you don’t need to add a beneficiary in advance. With UPI, you only need the recipient’s virtual ID, account number + IFSC, or UID number to initiate the fund transfer.